“Private Health Insurance gives consumers the peace of mind to know exactly when they can be admitted for surgery and other essential medical treatments and that is why the vast majority of consumers value it despite concerns about affordability,” according to Private Healthcare CEO Dr Rachel David.

Dr David said while this year’s average premium increase of 3.95% was the lowest in 17 years, no one liked to see premiums rise and the PHI industry had demonstrated its commitment to improving affordability by returning savings from medical device reform to health fund members.

“More than 13.5 million Australians hold PHI and over half of those have disposable incomes under $50,000 per annum. Many of these are full pensioners and superannuants who are making considerable sacrifices to maintain their health insurance.

“We know more than 80% of people with PHI believe they get value for money and in addition to the timing of medical treatment they cite choice of specialist for continuity of care and choice of hospital as the main reasons, however affordability is their greatest concern. (Ipsos)

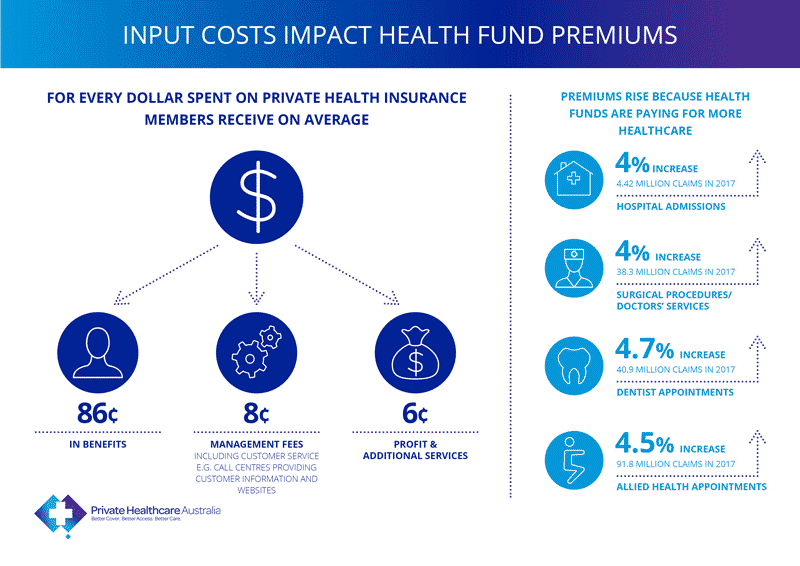

“There is only one reason premiums increase and that is because health funds are paying for more healthcare. The only way to put downward pressure on premiums as utilisation goes up is to address wasteful input costs – fraud, over servicing, inflated prices for medical devices, low value care.

“The key driver of premium growth is increases in input costs such as the cost of medical devices, hospital accommodation, and provider fees charged by medical specialists and allied health providers and health funds have limited control over these input costs.

“Affordability is an issue across the health system. Public hospitals have been guaranteed a 6.5% funding increase through the COAG process while in contrast this year’s average increase for PHI is 3.95%,” said Dr David.

In addition, a range of Government budget settings introduced over the last seven years have had a significant detrimental impact on the affordability of PHI for many Australians.

These include:

-

means-testing the rebate introduced in the 2009-10 Budget;

-

indexation to CPI, uncoupling the rebate from the cost of premiums, legislated in 2012;

-

removal of the rebate from LHC loadings, announced in 2009-10 Budget; and

- freezing the income thresholds for rebate eligibility at 2014-15 levels through 2020-21.

“The private sector continues to play a key role in Australia’s health system, performing nearly two-thirds of non-emergency surgery in Australia. 60% of all surgical procedures carried out in Australia are performed in private hospitals each year,” Dr David said.

“Overall, Private Health Insurance pays for 67% of all same day mental health treatment with or without ECT and 47% of all mental health admissions, 58% of all joint replacements and 61% of all chemotherapy treatments in Australian hospitals. 86% of retinal procedures take place in the private sector. In addition, under ancillary cover, health funds last year paid out nearly $2.66 billion for dental care, more than the Federal Government. Last year alone, health funds subsidised 40.9 million dental services.

“Profit margins have remained stable over the last decade running between 4.5 and 6%. This is a modest return when compared with other forms of insurance and significantly below the returns made by private hospital groups and medical specialist practices.

“Health funds are not hiding a pot of gold, they are committed to keeping premiums affordable for members and recognise the importance of working with hospitals, specialist health professionals and medical suppliers to establish premiums at a level which ensures members’ care can be funded if and when it is needed.

“Health funds are consistently paying out the highest percentage of the premium back to customers of all insurance types – an average of 86c in the dollar (it has been above 85% for 15 years). This compares with 67c for property insurance and 65c for general insurance.”

Dr David said consumers should carefully consider the value proposition of private health insurance before re-evaluating their health cover.

“These days, few people can afford the uncertainty of having to wait an unknown length of time to get a painful or disabling condition treated. Whether it’s a sporting injury that stops you driving your car, failing vision stopping you safely caring for family, or a child with an eating disorder who is missing school – these are all medical conditions that can’t wait without causing real social and economic consequences.”

Media contact: Jen Eddy 0439240755